Hubbard Radio Washington DC, LLC. All rights reserved. This website is not intended for users located within the European Economic Area.

If you have a Thrift Savings Plan account what did you do in December when the high-flying stock market, after wobbling a couple months, dropped big time? Finan...

It may be the difference between steak and hamburger or, worst case scenario, cat food. And you don’t have a cat!

So if you have a TSP account what did you do in December when the high-flying stock market, after wobbling a couple months, dropped big time?

Financial planner Arthur Stein has a number of federal clients including several who are TSP millionaires. He’s going to be my guest on our Your Turn radio show at 10 a.m. EST today. Listen at www.federalnewsnetwork.com or 1500 AM in the Washington, D.C. area. If you have questions for him email me before showtime at mcausey@federalnewsnetwork.com. In the meantime, Stein offered a preview:

Did you pass the test? Did you know you were taking a test?

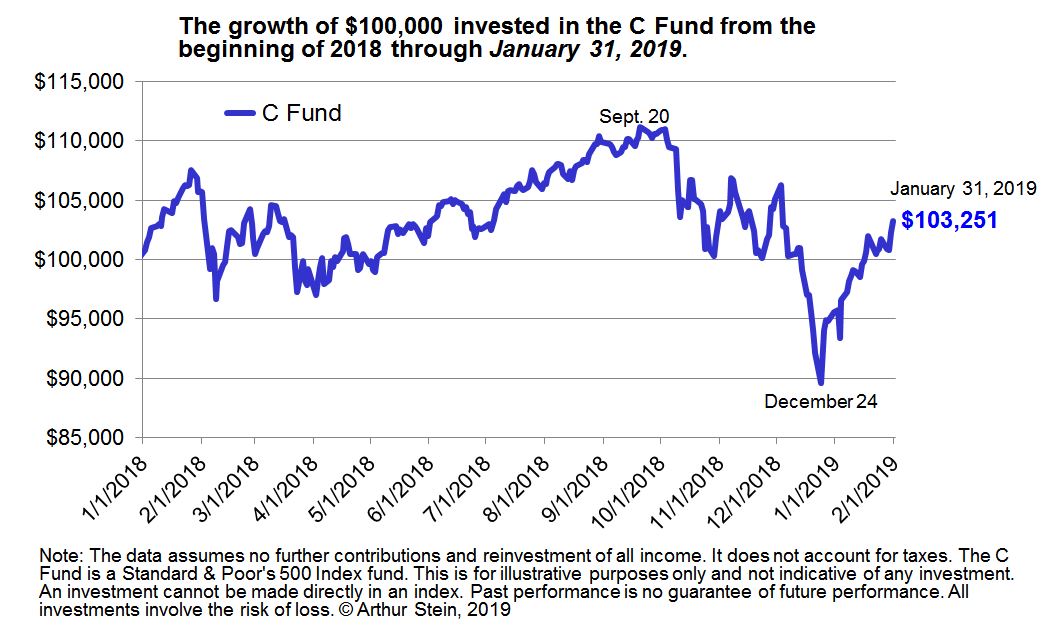

The test was in December, when the C Fund was down 9 percent for the month. The annual high for C Fund share prices was Sept. 20, and then it declined by 19.4 percent, hitting its lowest point for the year on Dec. 24.

That is what I call the Patient Investor Test: During the December declines, which investors held stock fund (C, S and I) investments and which investors transferred C, S and I balances to the G Fund? Who was a “market timer” and who was a “patient investor?”

Market timing — trying to sell in advance of a market decline and reinvest before stocks recover — is extremely difficult for even the best professional investors. It requires two accurate forecasts: when the market will begin declining and when it will begin recovering. It also requires nerves to buy stocks when the market is crashing and other investors are selling.

“Buy-and-hold” investors are the patient investors, content to stay fully invested during stock market declines. They see stocks as a good long-term investment and declines as temporary.

Historically, investors in well-diversified and well-managed stock portfolios did not have to buy and sell to profit. They only had to buy and hold for a sufficiently long period of time. Their patience was ultimately rewarded. Market timing wasn’t needed.

The last two months are a good example. December 2018 was a horrible month for the C Fund but in January 2019, the C Fund increased 8 percent. Patient investors who stayed in the C Fund saw a 12-month (January through December 2018) loss turn into a 13-month (January 2018-2019) gain of 3.3 percent.

All TSP funds benefited from a strong January performance, not just C.

| Total Returns Over Two Different Time Periods | |||||

| TSP Fund | G Fund | F Fund | C Fund | S Fund | I Fund |

| Type of Investment | Bonds — Short-term | Bonds — Intermediate | Stocks — Large US Companies | Stocks — Small and Medium Sized US Companies | Stocks — International |

| 2018 | 2.9% | 0.15% | -4.4% | -9.3% | -13.4% |

| 2018 Plus January 2019 | 3.1% | 1.2% | 3.3% | 1.3% | -7.7% |

| This is for illustrative purposes only. An investment cannot be made directly in an index. Past performance is no guarantee of future performance. All investments involve various risks, including loss of capital and volatility. Returns are not annualized. Returns rounded to tenths of a percent. Share prices include reinvestment of all income and do not account for taxes. Funds track these indexes: F — Bloomberg Barclays U.S. Aggregate Bond Index; C — Standard & Poor’s 500 Index; S — Dow Jones U.S. Completion TSM Index; I — MSCI EAFE Index. The G Fund does not track an index. | |||||

Former stock fund (C, S and I) investors who switched to the G and F funds in December now face a dilemma. Should they:

That is a tough decision.

Of course, past performance is no guarantee of future performance. It is possible that the stock markets may decline and not recover for an extended period of time. Stock investors should be prepared for these long declines. Stock market volatility, the constant increases and decreases in values, and sharp declines over short or long time periods are not a risk. They are a certainty. That is why patience is required.

According to well-known investor Warren Buffett, “The [stock] market is the most efficient mechanism anywhere in the world for transferring wealth from impatient people to patient people.”

By Amelia Brust

While in office, John Quincy Adams, sixth president of the United States, would awake at 5 a.m. and go skinny dipping in the Potomac River every morning.

Source: Mental Floss

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED