GettyImages/Federal News Network

Hundreds of federal and postal workers become retirement eligible every day. Although most don’t retire at the first opportunity.

Hundreds of federal and postal workers become retirement eligible every day. Although most don’t retire at the first opportunity, it’s a time when many people start looking at the best date(s) to pull that all-important plug.

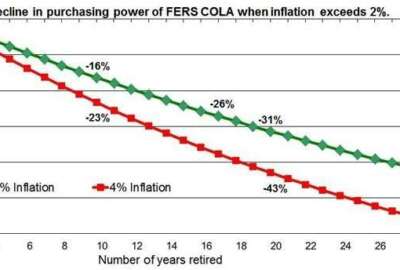

Most current civil servants are under the Federal Employees Retirement System. FERS workers pay into and get Social Security, and also have a more generous Thrift Savings Plan. But because of their smaller civil service annuity compared to those in the Civil Services Retirement System, who pay more for that benefit, timing is even more important.

So is there a “best” date for FERS workers to retire? The answer is yes but as far as the actual date goes, it depends.

Wednesday’s Your Turn radio show featured benefits expert Tammy Flanagan. She went through a checklist of things wanna be retirees should consider. It has both the questions and the answers to many key retirement considerations.

Tammy answered many question during the show but there were so many we couldn’t air them all. But she did answer them off-air, including this one from a fed named Jeff who had brain-twisting, but important, questions about FERS retirement timing. It should be helpful to other FERS workers looking for the best date or dates:

“As a FERS employee I’ve always heard that the best date to retire [to] maximize payout of annual leave would be late December in the year. As a GS-15, I normally hit my maximum annual leave contribution level from the 6.2% FICA tax in late October/late November. Lately, I’ve heard folks say that it might be best to retire in late October/late November so that your annual leave payout would not be subject to the 6.2% FICA tax. Of course, retiring in late December would mean that the annual leave payout would be taxed in the next year and I’m assuming would be beneficial since your taxable income would be lower due to retirement income. Do you have any thoughts on what situation would be best?”

Me, not a one — Tammy is different story. Fortunately or not, nothing in government is simple, which is why Tammy and I have jobs. Fortunately for Jeff, she’s got the surprising, naturally complicated answer:

“OK, let’s say his salary is $166,500 (maximum for a GS employee).

“Let’s say at the end of October, he has 408 hours of annual leave to cash out (240 from 2018 and 21 accruals of eight hours for 2019) at an hourly rate of $79.77 per hour worth $32,550 gross. If he is maxed out on the SSA FICA tax already, then he doesn’t have to pay 6.2% on this check, a savings of $2,018. However, if this lump sum pushes him from the 24% to the 32% federal tax bracket (for incomes above $160,726), then he will have to pay 8% higher federal income tax on this check, or $2,604 more federal income tax than if it is taxed at the 24% threshold.

“In addition, he would not earn the additional four accruals of eight hours of annual leave by working to the end of the year: $2,552.64 (gross amount). He will be paid at the 2019 rate for all of the leave instead of getting most of it at the 2020 rate — maybe 2.6% higher — or an extra $400 (gross). He would miss out on the 5% TSP matching for November and December: $1,387.50.

“So, all in all, he would save $2,000 but lose $7,000 (gross)! If he is maxed out on the SSA FICA tax already, then he doesn’t have to pay 6.2% on this check, a savings of $2,018. However, if this lump sum pushes him from the 24% to the 32% federal tax bracket (for incomes above $160,726), then he will have to pay 8% higher federal income tax on this check, or $2,604 more federal income tax than if it is taxed at the 24% threshold.”

Definitely food for thought.

By Amelia Brust

McDonalds is banned from opening any restaurant in Iceland, Bolivia, Iran, Macedonia, Ghana, Barbados, Montenegro, Jamaica, Iran and North Korea.

Source: The Telegraph

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED