Amelia Brust/Federal News Network

For many feds, the money they have in their Thrift Savings Plan will provide anywhere from one-third to one-half of their income. Most know that knowing when to buy...

One of the key questions on anybody’s retirement checklist is can I afford to live, decently, without a regular paycheck every two weeks for the rest of my life? If you can’t check that box, stick around for another couple of years until you can.

Will Social Security, savings (if any), and pension plan (if any) carry you possibly 20 or 30 years of retirement? The problem is many people don’t have more than a couple of weeks income in the form of savings. Many don’t have a pension plan. And if they are lucky enough to have one, chances are it is frozen at retirement. It will never change no matter how long you live and how high inflation goes. People who take Social Security as soon as possible (like age 62) will get a much reduced benefit than if they waited until age 70. But many literally can’t afford to wait, meaning many probably shouldn’t be giving up a regular pay check. Maybe ever!

Fortunately for most federal and postal workers Social Security and a retirement plan (which they partially paid for) will be available. CSRS retirees will get full cost of living protection. Those under FERS have a diet-COLA system. Last January CSRS retirees got a 5.9% COLA while those under FERS got 4.9%.

For many feds, the money they have in their Thrift Savings Plan will provide anywhere from one-third to one-half of their income. Uncle Sam matches up to 5%. That, plus the TSP low fees, make it one of the best 401k plans anywhere. More than 100,000 have become TSP millionaires. Most know that knowing when to buy and when to sell is a crap shoot, at best. Many bailed out of the TSP’s stock index funds during the Great Recession. Some are still waiting to come back. They missed the record recovery.

Given the current world situation, many TSP investors are bound to be having second thoughts. That makes this the perfect time to have financial planner Arthur Stein back on our Your Turn radio today. It begins at 10 a.m. EDT. It will be streaming on federalnewsnetwork.com or in the D.C.-Baltimore area on 1500 AM. He’s a well-known D.C. area financial planner (and congressional economist). Several of his regular clients are self-made TSP millionaires. If you have questions for him send them to me before showtime.

Meantime, he’s written this outline of what he will be talking about today.

TSP Investing and Market Timing (And COVID and Ukraine)

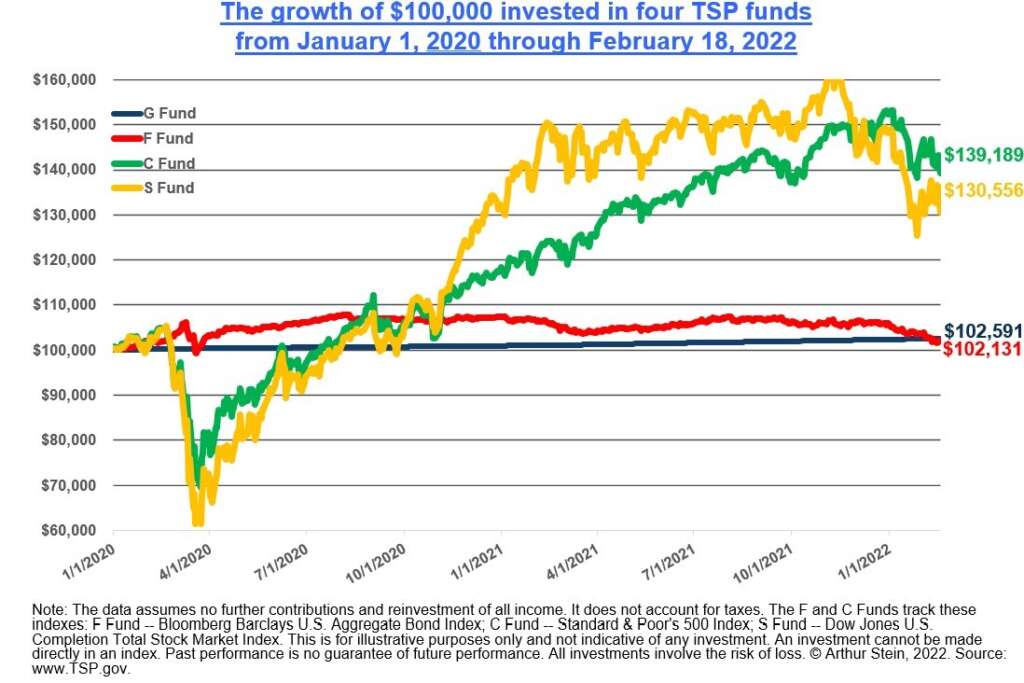

Some TSP investors try to use “market timing” to boost returns. “Market timing” means predicting stock market declines and advances and then transferring funds between the stock (C, S and I) and bond (G, F) funds in advance of what they predict will happen.

The COVID era (January 2020 and continuing) shows how difficult it is profit from market timing.

In March 2020, once the economic damage from the COVID epidemic became clear, the stock markets acted as expected: They crashed. From its previous high, the C Fund declined 34%.

But then something unexpected happened: U.S. stock markets quickly rebounded while U.S. and world economies were getting much worse. That meant market timers had to quickly reinvest in stocks when there was no economic evidence that it was the right time.

Now we know that holding the TSP U.S. stock funds during the worst of COVID was quite profitable. Even if market timers could have predicted COVID and the economic effects, they were probably not going to move fast enough to profit.

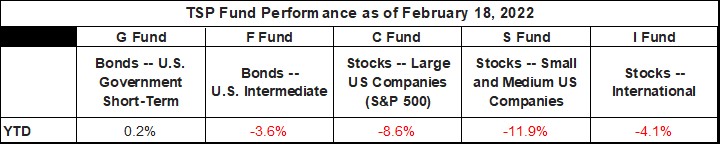

While COVID remains a powerful force in the world economy and our lives, it does appear that the situation is improving in 2022. So how did the stock funds react to the better news? By declining!

The difficulty (or impossibility) of profitably timing investments during COVID is relevant to current news about the Ukraine crisis. For instance, the Wall Street Journal ran this headline: “Stocks Finish Lower on Ukraine Tensions.”

Selling stock investments because of an expected invasion is market timing. But for market timers to profit, they first must determine if there will be an invasion of Ukraine, then the timing, how extensive the invasion will be and how long the fighting will last. Second, they need to know how the stock market will react to an invasion.

Let’s say our market timer is Russian President Vladimir Putin. He probably knows the answers to the invasion questions. What he wouldn’t know is whether an invasion would cause any additional market declines, how bad the declines would be and how long would the declines last. He needs to know the answer to those questions to buy back into the stock market at the right time. If he doesn’t buy back in at the right time, he doesn’t make a profit and may actually lose money.

Coffee beans are not actually beans. They are the seed inside the coffee fruit, which is small, red or purple, and commonly referred to as a cherry.

Source: Wikipedia

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED