Thinking retirement: When, where and why?

While your income will likely go down in retirement, moving to a more tax-friendly state could increase the cash value of your annuity.

The period between Dec. 1 and Jan. 3 is when the largest number of federal workers choose to retire. Timing it right means they can carry over the maximum amount of unused annual leave, get most or all of any January pay raise, and save on taxes in many cases.

But equally important for many is what next? Is there life after retirement? Does staying put or relocating make the most sense? While your income will likely go down in retirement, moving to a more tax-friendly state could increase the cash value of your annuity.

And there might be less snow to shovel.

At lunch earlier this week I talked with a long-time, recently retired fed who lives in the high-tax Maryland suburbs of Washington, D.C. He’s thinking about moving, maybe to Delaware, or North or South Carolina, largely because of their state tax policies. Like most people he picked a specific date to retire but his next step is whether to move or age in place.

Have you thought about where you will live in retirement, where you don’t want to live, like maybe your current home state? Do you live in a high tax state like New York, Massachusetts or Maryland? Have you checked out states with no sales or income taxes? Some don’t tax retirement benefits, others don’t tax Social Security benefits.

Why do so many feds, from President Donald Trump on down, change their legal residence from New York to Florida, or even New Jersey?

How much will your income drop going from work to retirement? When will you need to tap your Thrift Savings Plan account to make ends meet? Will you need it to fill in the gap between salary versus annuity, or is it something you hope to leave, in whole or part, for the kids?

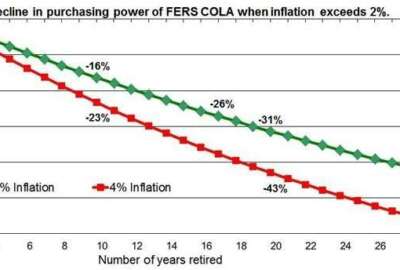

For many under the Civil Service Retirement System program, with its more generous annuity, money in the TSP is icing on the cake. For a majority of people under Federal Employees Retirement System, now the majority of all working feds, the TSP is an essential part of the package which includes the government annuity, Social Security and the TSP.

When in doubt, ask Tammy Flanagan. Many feel she wrote the book on federal retirement planning. She was a long-time fed and now operates her own fee-for-service business. Best of all, she’s our guest today at 10 a.m. EDT on our Your Turn radio show. The show is archived on our website so if you can’t catch it live on www.federalnewsnetwork.com or on 1500 AM in the Washington, D.C. area, you can always listen later and pass it along to a friend or coworker. Why listen? This is what Tammy says:

“Why do many federal employees have a difficult time knowing if they can afford to retire?

“There are three parts to FERS which means feds have to understand decisions that can impact the value of Social Security, FERS retirement benefits and withdrawal options of the TSP. That’s a lot to understand. They don’t know how much these benefits will be taxed: FERS has a small tax-free component, and is otherwise taxed as ordinary income (IRS Publication 721). Retirees file a W-4P for federal withholding and they can generally set up state tax withholding after their claim is adjudicated by the Office of Personnel Management.

“The TSP is 100% taxed as ordinary income unless it is coming from qualified Roth contributions, in which case it is tax-free. Federal tax withholding can be elected, but not state tax. Social Security is tax-free for many Americans, but not for most federal retirees.

“If your combined income is more than $34,000 for an individual return or $44,000 for a joint return, you will pay tax on 85% of the benefit for ordinary income tax. If you’re already getting benefits and then later decide to start withholding, you’ll need to submit a voluntary withholding request, also known as IRS Form W-4V. You’ll have the option of diverting 7%, 10%, 12% or 22% of your monthly benefits toward your income tax bill. You can also use the form to change your withholding rate or stop the withholding.

“Your combined income is your adjusted gross income, plus nontaxable interest and one-half of your Social Security benefits.

“On the state tax level, it depends whether your benefits will be taxed. Some states tax all of the benefits, some exempt federal retirement from state tax, some states don’t have a state income tax and some states tax FERS but not SSA.”

State Tax Roundup

Whether you stay in your current residence or move to another state often depends on family proximity, weather, housing prices and, very definitely, taxes. Some places may be much better, offering you a better lifestyle and more money to enjoy it.

Checkout this excellent state tax guide provided by National Active and Retired Federal Employees, which represents both active duty feds and retirees.

Nearly Useless Factoid

By Amelia Brust

The “proof” system for judging liquor’s alcohol content comes from 16th-century British tax collectors, who taxed spirits based on their alcohol content. Government officials would soak a gun pellet with the liquor and try to light it on fire, as “proof.” If it flamed, it was considered a proof spirit. but the flammability of liquor is temperature dependent, so in 1816 the government standardized its proof threshold to an alcohol level 12⁄13 the weight of an equal volume of distilled water at 11 degrees Celsius (51 degrees Fahrenheit).

Source: Encyclopedia Britannica

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED