How ’safe’ is playing it safe in the TSP?

When financial times get tough and a bear market rears its ugly head many Thrift Savings Plan investors head for the safety of the bond index F Fund or, more...

When financial times get tough and a bear market rears its ugly head many Thrift Savings Plan investors head for the safety of the bond index F Fund or, more likely, the super-safe never has a bad day G-fund. To many people, the U.S. Treasury-backed securities are the safest haven in an uncertain market.

During the Great Recession many TSP investors pulled out of the stock market (C, S and I funds) into the G-fund. Although the market bottomed out March 9, 2009 and rebounded with a vengeance, many investors never returned.

Art Stein, a certified financial planner, said there is safety and then there is “safety,” the latter actually used by people to mean a lack of volatility. Stein is a well-known Washington area financial planner with several TSP millionaires for clients. As the guest on today’s episode of the Your Turn radio show, he discussed the price to pay for safety:

“The terms ‘safe’ and ‘low risk’ are often used to describe the TSP bond funds (G and F). When TSP investors hear that the G and F funds are safer, many take it to mean that investing in those funds minimizes the risk of exhausting the balance in their TSP accounts before they die. Actually, they are safe one way but not so safe in other ways.

“What ‘safer’ actually means is that the G and F funds are less ‘volatile’ than the C and S stock funds. But that does not make them safer overall because volatility is not the only investment risk.

Investopedia defines volatility as a statistical measure of the dispersion of returns for a given security or market index … measured by using the Standard Deviation or variance between returns from that same security or market index. In other words, Stein said, the higher the volatility the more a stock or bond fund fluctuates in value compared to its average return.

“Lower volatility means the value of an investment fluctuates less [and] does not mean that an investment is generating a positive rate of return. An investment that lost 1 percent in value every month would be low in volatility, even as its value declined. Historically, for long-term investors in a well-diversified portfolio, a more important risk was the loss of purchasing power from taxes, inflation and lower returns.”

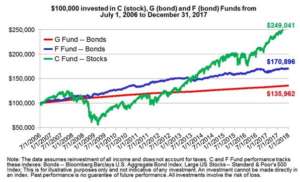

Stein offered this hypothetical example of high and low volatility, which illustrates the effects of investing $100,000 into the G, F and C Funds with no further contributions and no withdrawals:

The C Fund investment — in green — was more volatile than the F Fund investment — in blue — while the G Fund had no volatility. But after 11 and a half years the C Fund investment was worth 46 percent more than the F Fund and 83 percent more than G Fund investments. Patient C Fund investors would have been compensated for enduring much higher volatility over that 11-and-a-half-year period, Stein said.

Adding withdrawals makes the safety and volatility discussion more dramatic, he said. He offered another hypothetical example with three retirees who have have $10,000 in the TSP at the beginning of 1993. They each invest in one fund — Bill in the G Fund, Jack in the F Fund and Mary in the C Fund — and they annually withdraw enough to buy 2,000 First Class stamps after paying taxes of 30 percent.

“Why First Class stamps?” Stein asked. “First class stamps are an excellent proxy for inflation. They have provided exactly the same service every year since they were introduced. When the price increased, it was not accompanied by any increase in service or functionality.”

“Each retiree invests the same amount and withdraws the same amount. The amounts withdrawn varied as stamp prices increased but withdrawals were always the same dollar amount for each retiree. Volatility is much lower for the G and F Funds investors. Unfortunately, their account values steadily declined to zero,” Stein said.

Volatility is much higher for Mary’s C Fund investment, but the value of that investment would have been 37 percent higher after 24 years of withdrawals, he said.

“So which is riskier: Mary’s C Fund (stock) investment or Bill and Jack’s G and F (bonds) Fund investments?” Stein asked.

To hear his answer, turn to Your Turn today at 10 a.m. on Federal News Radio or 1500 AM in the D.C. metro area. Questions can also be called into 202-465-3080 or emailed to mcausey@federalnewsradio.com before the show.

Nearly Useless Factoid

By Amelia Brust

During the Great Famine in Ireland, Khaleefah Abdul-Majid I — also known as Abdulmejid I — sultan of the Ottoman Empire in modern-day Turkey offered £10,000 to aide Irish farmers. But Queen Victoria, who was then the country’s monarch, asked him to only send £1,000 so as not to make her own contribution of £2,000 seem paltry by comparison. The sultan also secretly sent ships of food to Ireland, which English courts unsuccessfully tried to block from reaching port.

Sources: Irish Central

Copyright © 2025 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED