President Donald Trump/ (AP Photo/Evan Vucci)

Senior Correspondent Mike Causey says the greatest fear of retirees who don't get a pension from work or an inflation adjustment is running out of money.

If you ask most people their greatest fear about retiring, they would probably say running out of money. Especially if they don’t get a pension from work, or if the benefit they eventually receive is fixed with no inflation adjustments. Ever.

Financial planner Arthur Stein says the running-out-of-money fear is common among federal workers planning for retirement or who have already retired. Understandable, he says, but wrong. The good news, he says, is that while former feds may run low on money, they will never run out of money. An important difference to be considered when prepping for retirement:

“Federal retirees will never run of out income,” says Stein. “They will always receive monthly annuity (pension) payments from the federal government. FERS employees will also receive Social Security payments. Both these payments are guaranteed to last the lifetime of the retiree and offer annual cost-of-living adjustments (COLA).”

That inflation protection is virtually unknown in pension plans in the private sector. Somebody who retired on $800 a month in 15 years ago is still getting $800 a month today.

Stein, who has lots of active and retired federal clients, says “Retirees need to worry about a different risk: exhausting their investments. At some point during a retirement, most retirees will need to start withdrawing funds from their investments to supplement their annuity and Social Security payments. Investments are not guaranteed to last a lifetime. If too much is withdrawn, the investments are exhausted, and income from investments stops. The retiree is only left with the annuity and Social Security, which forces them to reduce expenditures no matter what their actual needs.”

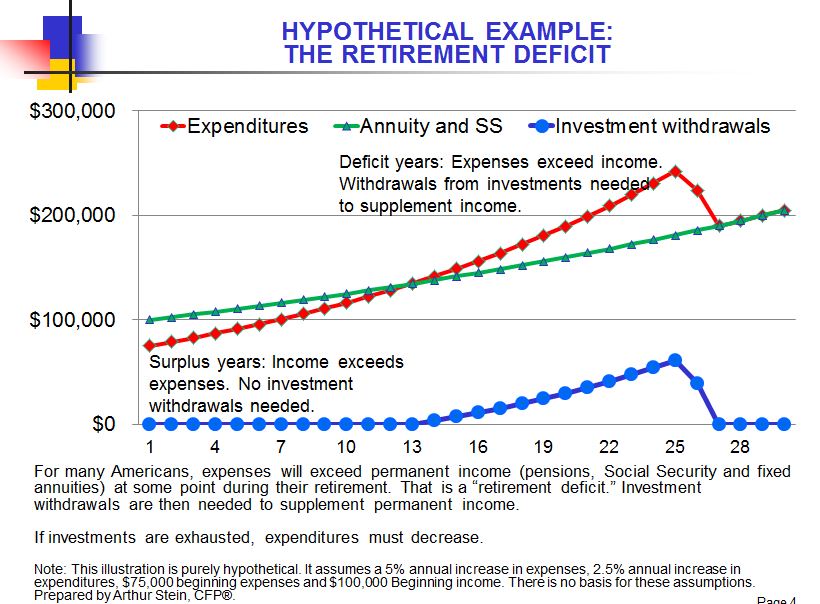

“Here is a hypothetical example where retirement …

• Income exceeds expenditures for the first 13 years (surplus).”

• Expenditures exceed the retiree’s annuity and Social Security payments beginning in year 14 (deficit).”

• Investment withdrawals then supplement annuity and Social Security payments.”

• Investments are exhausted in year 27, withdrawals end and expenditures have to decrease.”

All this means that investments in the Thrift Savings Plan are important to workers and retirees under the CSRS program, where benefits are fully indexed to inflation. And income from TSP investments is absolutely critical for the majority of current workers who are under the FERS program. FERS is a combination of federal annuity, Social Security and your TSP investments (plus the available 5 percent match from the government). But because its benefits are not fully protected from inflation, which exceeds 2 percent a year, having a sizable TSP account is essential to most FERS retirees — unless they hit the lottery big time.

Today at 10 a.m. on our Your Turn show, Stein will talk about how long your investments might (and should) last during retirement. If you have any questions, please email them to me before show time: mcausey@federalnewsradio.com. You can listen in the D.C. area on 1500 AM or anywhere, from your computer, at FederalNewsRadio.com The show will be archived (like all our Your Turn reports) so you can listen later, listen again or refer it to a friend.

By David Thornton

Lobsters taste with their feet. Chemosensory leg and feet hairs identify food.

Source: Time

Copyright © 2025 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED