Hubbard Radio Washington DC, LLC. All rights reserved. This website is not intended for users located within the European Economic Area.

Senior Correspondent Mike Causey recently received an email from a listener with $1.2 million in the Thrift Savings Plan and made on his second move of funds la...

The following column was submitted by Arthur Stein, a Washington, D.C.-area based certified financial planner with more than two decades of experience.

Mike Causey recently received the following email from a listener, let’s call him Tom:

“I have [$]1.2 million in the [Thrift Savings Plan] as of yesterday. I am 57 and in my 31st year as a government employee … I left my TSP 100 percent in the C Fund for 27 years. Four years ago, I went to the Lifecycle 2040 plan. In only my second move, last September I moved to the Lifecycle 2020 plan as I was worried re: trade, Trump, etc.”

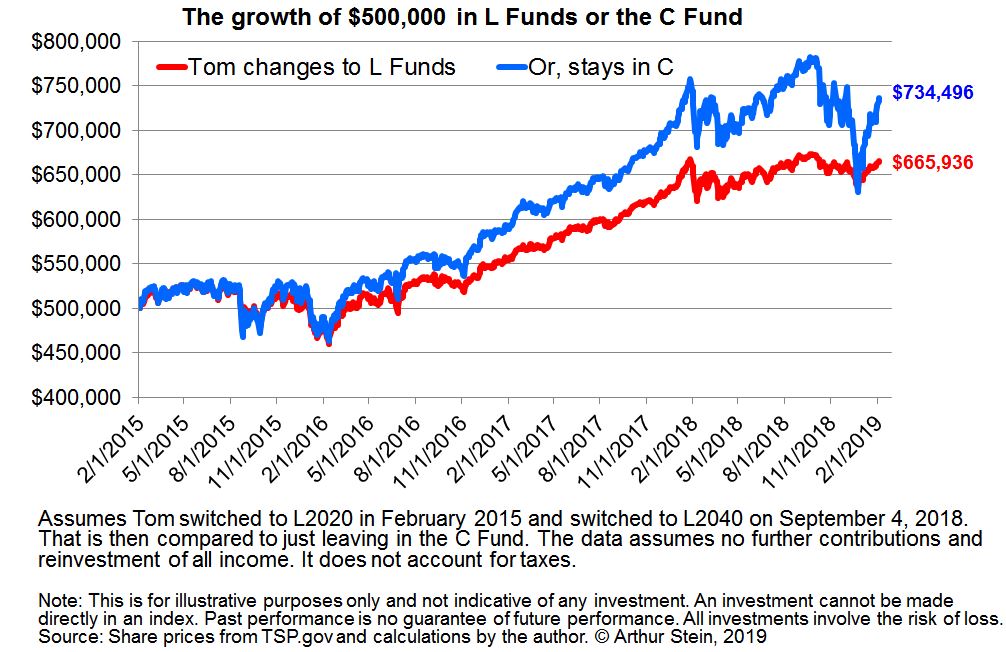

Questions: Did the transfer to the L funds generate a higher return for Tom? Was it in some way “safer?”

By using share prices downloaded from www.TSP.gov and assuming Tom had $500,000 in the TSP four years ago, it is possible to calculate the differences between leaving his TSP balance completely in C, or in February 2015 transferring from C to L2040 and in September 2018 transferring to L2040.

The following graph illustrates these two alternatives.

Staying in the C Fund would have resulted in a higher return. After four years, Tom would have had 10.6 percent more if he had left his money in the C Fund.

There were only 60 days when the L Fund investments were worth less than the C Fund investment. Fifty-nine of those days occurred in 2015, the first year of the comparison, while the remaining day was Dec. 24, 2018. But the L Fund advantage only lasted that one day.

On a percentage basis, the L Fund strategy only had a higher value on 0.06 percent of the days examined. The L Fund investments appear to be less volatile. In that way, they are “safer.”

Which was the better strategy? It is difficult to say because TSP participants have different goals, needs and investment concerns. But we can say that long-term TSP investors face a dilemma.

Invest for lower volatility and a lower chance of losing principal (safety) but with a higher chance of a decline in purchasing power. Or, the higher potential growth historically offered by stocks, accepting greater risk for the opportunity to increase purchasing power.

Each investor must choose.

By Amelia Brust

Manatees are part of the Sirenia animal order, and their closest living relative is the elephant.

Source: Smithsonian Mag

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.