Hubbard Radio Washington DC, LLC. All rights reserved. This website is not intended for users located within the European Economic Area.

Fast approaching is the health benefits open enrollment period from Nov. 11-Dec. 9, when workers and retirees should shop carefully for the best deal for them a...

Also fast approaching is the health benefits open enrollment period from Nov. 11-Dec. 9, when workers and retirees should shop carefully for the best deal for them and their families. Premiums in many plans are going up. But some are actually reducing premiums. Many experts say that picking the plan best for you can save $1,000 to $2,000 in premiums next year and $1,000 and $2,000 in taxes in some cases.

Although it’s comforting to stay in the same health plan year after year, things change. You may have changed, your health plan may have changed. And the options to choose have certainly changed. One that often requires a change is turning 65 years old and understanding the link between the Federal Employees Health Benefits plans and Medicare.

Picking the right date can raise the cash value of your lump sum annual leave payment. It can also lower your tax bill. Dec. 31 is generally the best date for people retiring under the Federal Employees Retirement System. Jan. 3 is usually the best move for those retiring under the Civil Service Retirement System at the end of the 2019 leave year. Missing the best dates, even by a day or two, can make a lot of difference.

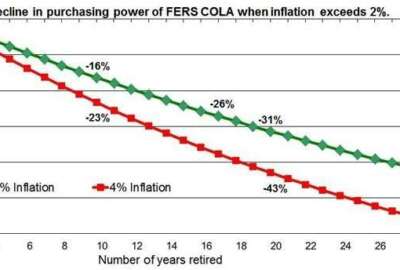

Retirees with Medicare Part B have some excellent choices of FEHBP plans that provide incentives and cash to help cover the cost of the Part B premium. Military retirees can save a lot of money by suspending — not dropping — their FEHBP plan in 2020 and using TRICARE for Life, which has a $0 premium as the cost was paid by their service.

So what makes those specific dates the best dates to retire? And what about using Medicare to reduce or eliminate your out of pocket medical expenses? What’s magic about the best dates to retire, and the link between Medicare and the FEHBP. That’s what we hope to find out today on our Your Turn radio show. Our guest is benefits expert Tammy Flanagan. She was a long-time fed now retired with her counseling service. She’s also a columnist for GovExec Magazine.

Today at 10 a.m. Tammy is going to talk about the best dates and Medicare and the FEHBP. The show is live at 10 a.m. on www.federalnewsnetwork.com or on 1500 AM in the Washington, D.C., area. If the boss won’t let you listen — some agencies encourage it — at the office, the show will be archived so you can catch it later or pass it on to a friend and coworker. Questions for Tammy should be emailed before showtime to mcausey@federalnewsnetwork.com. Listen a little now and save a bundle later.

By Amelia Brust

One of the earliest methods of pregnancy testing, the “rabbit test,” used in the 1920s involved injecting a female rabbit with a potentially pregnant woman’s urine. If positive, the urine would have the hormone human chorionic gonadotropin, or hCG, and that rabbit’s ovaries would also start changing. But to check, originally scientists had to kill the rabbit. Eventually they learned how to avoid that step, but hCG levels are still a part of modern-day pregnancy testing.

Source: Snopes

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED