(AP Photo/Elise Amendola)

While there is a lot of interest in those who are self-made Thrift Savings Plan millionaires, the fact is most investors will never hit seven-figure status.

While there is a lot of interest in the number of people who are self-made Thrift Savings Plan millionaires, the fact is most of the 5.6 million investors in the federal 401(k) plan will never hit seven-figure status.

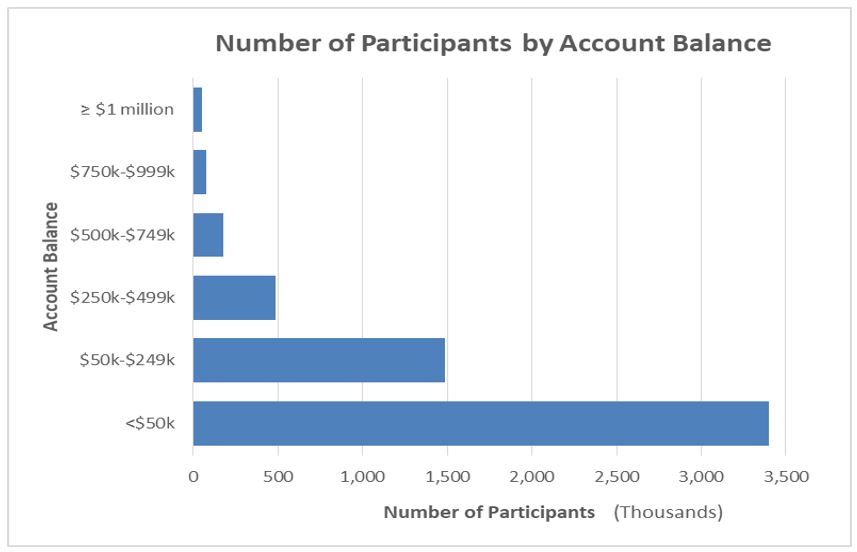

As of Dec. 31, 2019, there were 49,620 members of the Millionaires Club, including one with a balance of $7,396,476.29. The vast majority of people in the program, active and retired, will never reach that magic number.

Not that there’s anything wrong with that! Put away the hair shirt, cease your guilt trip. Not many people manage to accumulate a seven–figure nest egg even after working, saving and investing for 30 or 40 years. But while the big bucks are fascinating, the real story is how many long-time, working stiff civil servants, in dozens of different jobs, federal agencies and locations, are knocking on the door with eye-popping six-figure accounts.

Those 49,620 TSP millionaires were current and retired air traffic controllers, CIA operatives, federal judges and their clerks, poultry inspectors, rocket scientists, border patrol officers and scientists.

At the same time, 5,628,369 people did not have $1 million or more in the TSP. But some are so, so close and if the bull market keeps rolling along many will qualify each month of this year. We’ve talked with three who are on target to hit it this winter, and another investor who will hit the $2 million mark in April — he hopes.

Naturally, most of the publicity concerning TSP is focused on those at the top. A few of them brought the money with them from jobs outside government, like (very) successful corporate and defense attorneys who became federal judges, or political appointees who came from Wall Street or Hollywood. But the real story to many people is the more than 74,000 rank-and-file civil servants have account balances between $750,000 and $999,000, and why. Or what about the more than 176,000 whose accounts range from $500,000 to $749,000? By now, many of them, thanks to the continued bull market, have moved up a bracket or achieved millionaire status.

This means that in addition to Social Security (based on covered earnings and contributions), and their Federal Employees Retirement System or Civil Service Retirement System annuity they will have a third source of income — after tax payments from their TSP accounts — to live off of in retirement. Or they can leave it as part of their estate.

But back to the “why?” part.

Many people say the difference between TSP savers and regular, private sector 401(k) plan savers is the government match. Over time, with compounding, that can make a huge difference. Take this 24-year-long fed who has been tracking and comparing his TSP with his former brother-in-law’s private 401(k) plan:

“Right out of college my brother-in-law and I got jobs. He married my sister, although they are now divorced. I joined the government, Defense Department. He went with several DoD and government contractors. For a while he made more than I did, but got less annual leave and fewer holidays. The big difference we noticed was the match. I got 5%. He got nothing at two places, 3% at another. The bottom line is we had the same or certainly similar investment options. My fees were lower, but the primary difference was the match. I’m $49,000 and change ahead of him today with [essentially] the same investments.” — Happy Sam

Regardless of how much they have in their TSP accounts, these people are both lucky and smart — lucky, or wise, because they chose federal employment which, unlike many private employers still offers a defined benefit retirement plan linked to inflation, and a 401(k) option which offers most the chance to get a tax-deferred 5% match from their agency. They put in 5%, Uncle Sam matches. The successful investors are also in it for the long-haul. Those with accounts ranging from $250,000 to $499,000 have been investing an average of 21.15 years. Those with $500,000 to $749,000 have been investing an average of 24 years while those with bigger accounts have been investing steadily — primarily if not exclusively in the stock-indexed C, S and I funds — anywhere from 24 to 29 years. Most stuck with their investments through good times and bad. During the Great Recession they continued to buy C, S and I shares that had plummeted as much as 40%, meaning they bought more with less.

Staying the course during the normal ups and downs of the stock market usually makes sense over time, and a full career of investing. But in the short term it can be tough.

Last week’s column about the fast-growing TSP millionaires club prompted some fascinating responses from readers, several of whom are at past the seven-figure level.

By Amelia Brust

In October, engineers in Denmark managed to move the 120-year-old, 1,000-ton Rubjerg Knude lighthouse about 263 feet inland on a pair of custom roller blades, to save it from rising tides that were eroding the structure. The process took 59 hours and the lighthouse moved at 0.001 mph.

Source: MentalFloss

Copyright © 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

Mike Causey is senior correspondent for Federal News Network and writes his daily Federal Report column on federal employees’ pay, benefits and retirement.

Follow @mcauseyWFED